Hearson, M, 2018. Transnational expertise and the expansion of the international tax regime: imposing ‘acceptable’ standards. Review of International Political Economy 25(5):647-671. We are living through a period of instability and change in the international tax regime, perhaps unprecedented in its depth and duration. It’s driven by economic and political changes, such as austerity politics, the digitisation… Continue reading Transnational expertise and the expansion of the international tax regime

Tag: United Kingdom

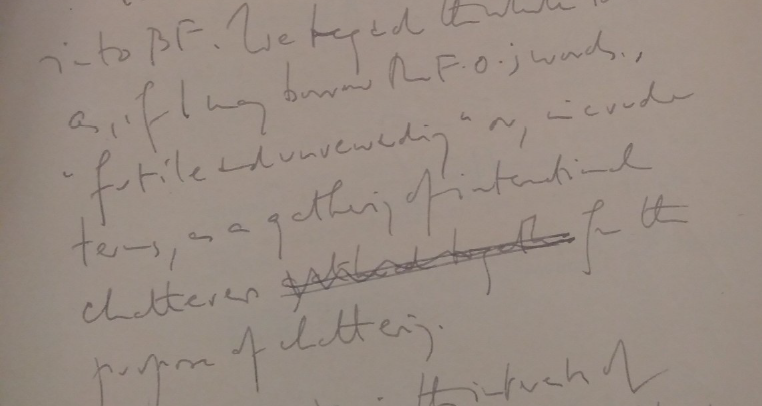

“A gathering of international chatterers for the purpose of chattering.” The birth of the OECD’s Committee on Fiscal Affairs.

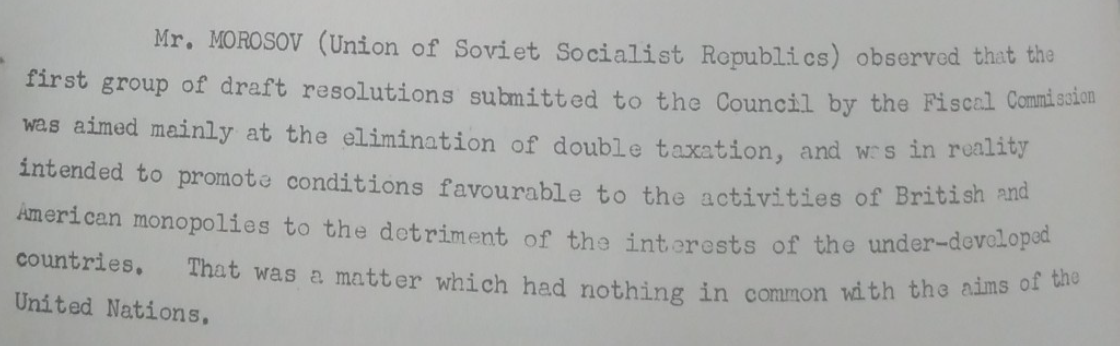

In my previous post I explored the United Nations’ brief post-war flirtation with a Fiscal Commission, which came stuttering to a halt in 1951 due, it seemed, to the lack of a compelling purpose that might have motivated states to fight to retain it. The United Kingdom had supported a Russian proposal to wind up… Continue reading “A gathering of international chatterers for the purpose of chattering.” The birth of the OECD’s Committee on Fiscal Affairs.

“Futile and unrewarding”: the wilderness years of the international tax regime

Almost all histories of the international tax regime begin with the League of Nations: from the model conventions issued by its Fiscal Committee in 1928, to the Mexico and London draft model conventions. The latter was agreed by a group of primarily European countries in 1946 at Somerset House, just across the road from where I… Continue reading “Futile and unrewarding”: the wilderness years of the international tax regime

The Colombia UK tax treaty: 80 years in the making

Hearson, M, 2017. The UK-Colombia Tax Treaty: 80 Years in the Making. British Tax Review (4):375-384. Today at 2.30pm, the UK parliament’s Third Delegated Legislation Committee will debate tax treaties with Lesotho and Colombia. It will be interesting to see how much debate really takes place, a matter on which I’ve commented before once or… Continue reading The Colombia UK tax treaty: 80 years in the making

Some follow-up on parliamentary scrutiny of the UK-Senegal treaty

As my last post anticipated, the ratification of the UK-Senegal tax treaty was debated in parliament last week. It was great that a debate on the impact of a tax treaty between the UK and a developing country happened at all. Some important issues came up: What is the role of the Department for International… Continue reading Some follow-up on parliamentary scrutiny of the UK-Senegal treaty

Questions the opposition should ask about the new UK-Senegal tax treaty

Back in February, the UK and Senegal signed a bilateral tax treaty. The treaty is up for ratification this week, so I thought it time to take a look. Ratification happens through the delegated legislation committee, and entails very little debate. The last time a treaty between the UK and a developing country was ratified,… Continue reading Questions the opposition should ask about the new UK-Senegal tax treaty