Back in February, the UK and Senegal signed a bilateral tax treaty. The treaty is up for ratification this week, so I thought it time to take a look. Ratification happens through the delegated legislation committee, and entails very little debate. The last time a treaty between the UK and a developing country was ratified, I thought it was a shame that there had not been more discussion, which is why I’m writing in advance this time. I’ve also commented in the past, as did ActionAid and Mike Lewis, on the Danish treaty with Ghana.

So what questions might an interested Shadow Financial Secretary ask during this ratification debate? Here are three suggestions.

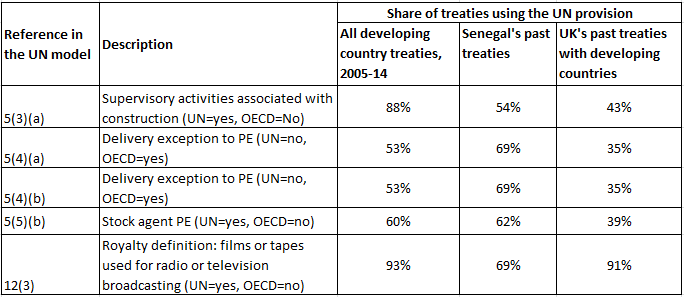

First, they might ask about a few of the provisions within the treaty that disadvantage Senegal and that seem to go against modern negotiating trends. The table below shows some provisions within the UK-Senegal treaty that follow the OECD model (which favours the developed country) rather than the UN model (which is supposed to reflect a good balance in a negotiation between a developed and a developing country). The first of the three percentage columns shows that these are all provisions that have been included in the majority of treaties signed by developing countries in recent years; the second shows that they are included in the majority of Senegal’s treaties; the third shows how often the UK has conceded them to developing countries.

The treaty is particularly unusual in that supervisory activities associated with a building site in Senegal conducted by a British firm will not be taxable in Senegal, nor will royalties paid to the UK for radio and TV programmes broadcast in Senegal. Both of these provisions are included in around 90% of tax treaties signed by developing countries, but are omitted from this one. It would certainly be interesting to ask why.

Second, it is notable that this treaty does not include a clause permitting Senegal to tax fees for technical services paid to the UK. This is something that Senegal’s chief negotiator has for years advocated strongly for, including in this submission to the UN tax committee [pdf]. The UK has many older treaties with developing countries that include this provision, but more recently it seems to have changed position, opposing them. In this negotiation, it looks like Senegal made a concession on this point. This is a contentious issue at the UN tax committee, but the committee – which has members from the UK and Senegal – looks to be heading towards including it within its model treaty. It would therefore be very interesting for politicians to debate the UK’s position.

Third, the ratification debate on this treaty could be an opening for a broader discussion of what the UK aims to achieve through its tax treaties with developing countries. To set this in context, in the chart below, every point represents a tax treaty signed by a developing country, with the vertical axis showing how source-based it is (that is, how much its content permits the developing country to tax investors from the treaty partner). The higher the point, the more the balance of the treaty tends towards the developing country’s favour. There’s a leisurely upward trend.

The UK’s agreements with developing countries are in red, while Senegal’s are in blue. The UK-Senegal treaty is purple. While it looks to be about average for both countries, it is certainly one of the more restrictive (“residence-based”) treaties signed by developing countries in recent years. This seems to be typical of treaties signed recently by the UK, but a worse deal for Senegal than it has obtained for a few years. The implication that the UK is one of the toughest tax negotiators with developing countries is surely worth political interrogation, at a time when its Department for International Development is urging developing countries to improve tax collection.