Almost all histories of the international tax regime begin with the League of Nations: from the model conventions issued by its Fiscal Committee in 1928, to the Mexico and London draft model conventions. The latter was agreed by a group of primarily European countries in 1946 at Somerset House, just across the road from where I… Continue reading “Futile and unrewarding”: the wilderness years of the international tax regime

Tag: United Nations

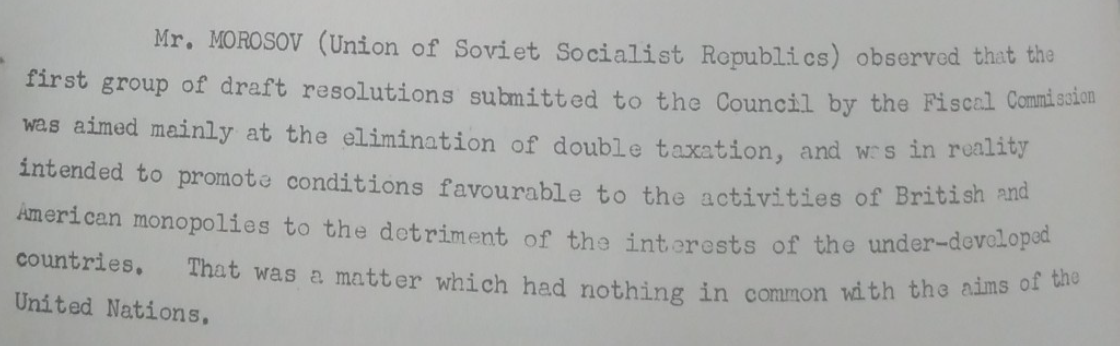

Developing Countries’ Role in International Tax Cooperation

Over the past year I’ve worked with the secretariat of the Intergovernmental Group of 24* on a paper that discusses how developing countries could engage with a range of international tax cooperation issues. The paper can be downloaded here: Developing countries’ role in international tax cooperation [pdf]. The G-24 plays a caucusing role for its… Continue reading Developing Countries’ Role in International Tax Cooperation

Some follow-up on parliamentary scrutiny of the UK-Senegal treaty

As my last post anticipated, the ratification of the UK-Senegal tax treaty was debated in parliament last week. It was great that a debate on the impact of a tax treaty between the UK and a developing country happened at all. Some important issues came up: What is the role of the Department for International… Continue reading Some follow-up on parliamentary scrutiny of the UK-Senegal treaty

Questions the opposition should ask about the new UK-Senegal tax treaty

Back in February, the UK and Senegal signed a bilateral tax treaty. The treaty is up for ratification this week, so I thought it time to take a look. Ratification happens through the delegated legislation committee, and entails very little debate. The last time a treaty between the UK and a developing country was ratified,… Continue reading Questions the opposition should ask about the new UK-Senegal tax treaty

The tax treaty arbitrators cometh

Next month sees the results of the OECD’s Base Erosion and Profit-Shifting project, as well as a discussion at the UN tax committee on alternative dispute resolution in tax treaties. India has apparently vetoed the inclusion of mandatory binding arbitration by default in the OECD model tax treaty, and it remains an optional provision within… Continue reading The tax treaty arbitrators cometh

Is tax treaty arbitration really a bad thing for developing countries?

I’m at the United Nations tax committee annual session this week, where I’ve learnt that I have to be careful what I write here, after a couple of posts from this blog were included in an input document [pdf]. Erk! I’ve been taking the opportunity to discuss with delegates the recent article [£] by the… Continue reading Is tax treaty arbitration really a bad thing for developing countries?