Over the past year I’ve worked with the secretariat of the Intergovernmental Group of 24* on a paper that discusses how developing countries could engage with a range of international tax cooperation issues. The paper can be downloaded here: Developing countries’ role in international tax cooperation [pdf].

Over the past year I’ve worked with the secretariat of the Intergovernmental Group of 24* on a paper that discusses how developing countries could engage with a range of international tax cooperation issues. The paper can be downloaded here: Developing countries’ role in international tax cooperation [pdf].

The G-24 plays a caucusing role for its members in the IMF and World Bank, and so tax cooperation is becoming increasingly important for it as those organisations’ profile in tax work increases. There were some interesting presentations at the G-24’s last technical group meeting in February, and its most recent ministerial communique [pdf] includes the following statement, a mix of welcoming current initiatives and noting areas where they are insufficient for emerging markets and developing countries (‘EMDCs’):

We welcome ongoing initiatives on international tax cooperation such as the Automatic Exchange of Information (AEoI) initiative and the Base Erosion and Profit Shifting (BEPS), and call for a framework that ensures effective participation of EMDCs. We support the development of a digital global platform with least compliance cost for implementation of AEoI. We appreciate the work of the UN Tax Committee and encourage multilateral support to upgrade the Committee to an intergovernmental body to enhance the voice of EMDCs on international tax policy matters. We also call for more attention to developing fair tax rules to guide the taxation of multinational corporations and for international cooperation to prevent harmful international tax competition, negative spillovers from shifts in tax policies in major countries, and illicit financial flows.

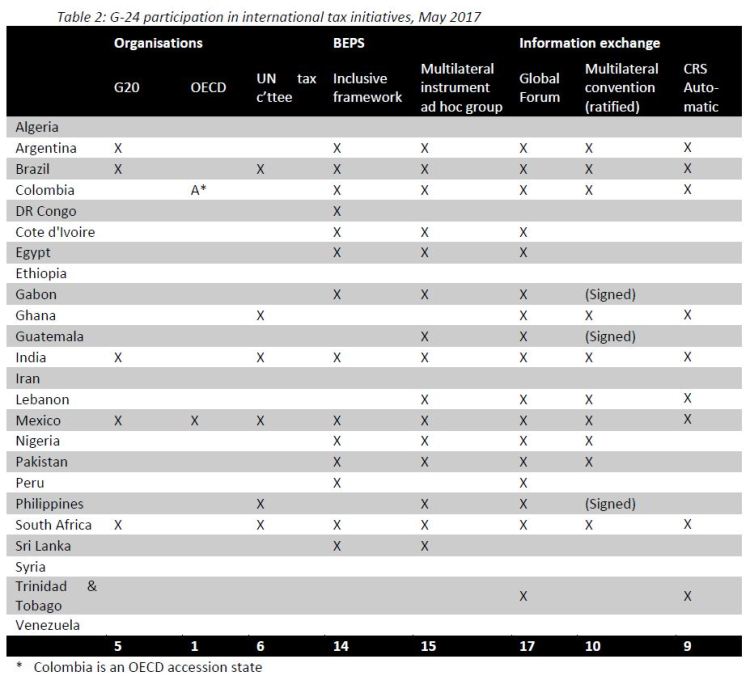

One of the interesting elements of this project was the diverse positions and interests within an equally diverse group of ‘EMDCs’. Below, for example, is a table showing participation in international tax organisations and institutions. This was such a moving target that we had to set a ‘freeze date’ of 25th May 2017.

I hope the report provides a good overview of the state of play and issues involved on that date. Below is the text of the recommendations section, which gives a flavour of the document.

The G-24 has highlighted the importance of effective international tax cooperation to support developing countries’ efforts to mobilise domestic resources, so that they can achieve their development goals. It could build on this recognition by setting out to develop a pro-active agenda for international tax rule reform that meets the needs of developing countries, and identify different international forums through which to achieve it. G-24 members could work together within existing forums such as the UN tax committee and OECD to put their issues of concern on the agenda. The UN tax committee’s potential has yet to be fully realised by developing countries, and there may also be new opportunities created by enhanced participation in OECD initiatives. G-24 members could strengthen their engagement by enhancing national political oversight of UN and OECD tax work, as well as advocating a stronger, upgraded UN tax committee when the opportunity next arises.

On tax avoidance and evasion, G-24 members could consolidate their participation in multilateral conventions on information exchange and mutual assistance, and could share their knowledge and experiences in this area to build each other’s capacity to benefit from their participation, as well as to identify reforms to international tax standards that might reduce the administrative hurdles to benefit. Where necessary, this could lead to alternative, but compatible, standards in areas such as transfer pricing and tax treaties that give a greater share of the tax base to developing countries.

As some G-24 countries are capital-exporters to other developing countries, they could take up the IMF and OECD’s recommendation to perform ‘spillover analyses’ of the main aspects of their tax systems that have the potential to adversely affect other developing countries’ tax revenues, whether by encouraging tax competition or increasing incentives for tax avoidance. Also with regard to tax avoidance, G-24 members could share experiences across regional economic groupings such as ASEAN and MERCOSUR to advocate codes of conduct on tax competition, as well as working through ECOSOC for the adoption of the UN tax committee’s proposed code of conduct on exchange of tax information.

Above all, the G-24 provides a political platform for forging common views on international development issues among developing countries, in which tax coordination is a main concern. It is able to work with the OECD within its inclusive framework, and a number of G-24 members are now participating in many of its initiatives. It can also support the efforts of the UN and other forums in which developing countries can more actively engage so that they can benefit more effectively from international tax rule reforms and cooperation. A sustainable approach to international tax cooperation in the long term requires international institutions that reflect the increasingly diverse needs of countries with an interest in international tax standards.

*Just as there are 19 countries in the G-20, and 134 countries in the G-77, there are now 26-and-a-half countries in the G-24. The ‘half’ is China, which has the status of ‘special invitee’.