As I write this post, the new UN tax committee is in closed session, choosing its new chair. This first act of the committee feels like it will have an important tone-setting impact. There is much speculation about who is the preferred candidate among members from OECD countries, and an assumption that those members will have arrived with a pre-agreed nominee. In contrast, while one name in particular among the members from developing countries is being mentioned in informal chat, there does not seem to be a consensus, a consequence perhaps of politics and of the fact that these members do not know each other so well. This dynamic is especially important, because the composition of the committee has changed, with members from the OECD now significantly outnumbered for the first time.

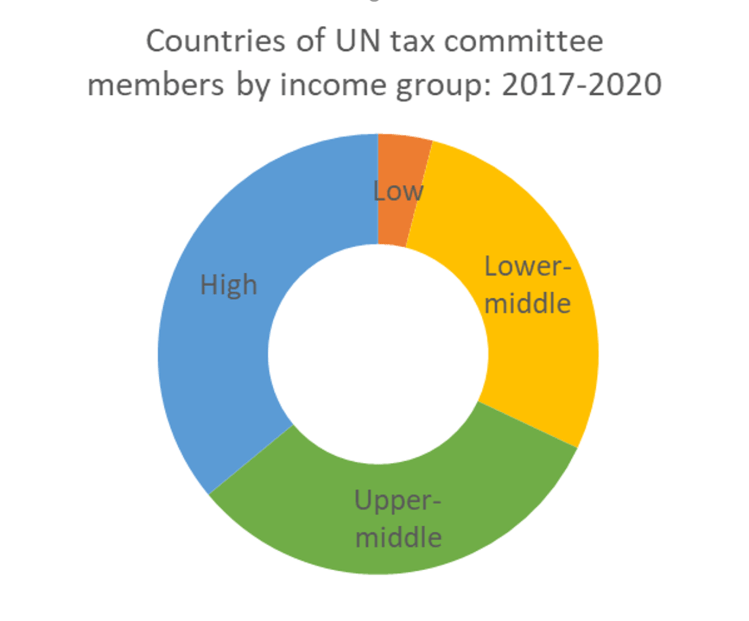

The last committee was finely balanced, with 12 members from OECD states and 13 from outside the OECD. Having said that, four more were G20 members, meaning that 16 of the committee came from countries that had seats at the high table of international tax rulemaking, while only nine were outside that particular tent. Looking at it by country income group, 13 were from high income countries, despite the UN tax committee’s developing country remit.

If we consider the members personally, eight of them were officers of an OECD tax committee, including the chair and vice-chair of Chair of OECD Working Party 1 on Tax Conventions and Related Questions, two bureau members of OECD Working Party No. 6 on the Taxation of Multinational Enterprises, and two bureau members of the OECD’s Committee on Fiscal Affairs itself. Many of these eight were among the most vocal and active members, chairing the UN tax committee itself and several of its subcommittees.

This time around, I can count only eight members from OECD countries, and a clear majority of members from developing countries. There’s a caveat, however, which is that, as the OECD has invited more countries to participate in its Committee on Fiscal Affairs, a further seven members come from countries that are CFA participants or associates. There are now only five committee members who are officers on OECD committees, including both Vice-chairs of WP1 and two CFA bureau members. It’s a measure of how things are changing that one of these is from Argentina, which is not yet an OECD member. All of this means that, largely as before, only 10 of the 25 committee members come from countries that do not have a seat in the OECD and G20’s main tax discussions. Many of those ten, of course, are members of the Inclusive Framework and other OECD forums.

So there is still some truth to the idea that the UN tax committee is essentially a forum in which many of the same people discuss many of the same topics, but with a different mandate and to some extent a different balance of power. For example, some UN committee members from OECD countries had reputations for actively supporting positions that differed from the OECD consensus, but were favoured by developing countries, in UN deliberations.

How ‘equal’ the ‘equal footing’ granted by the OECD is in practice is a question often raised. But it is also worth noting that at the UN committee, not all members have equal influence. Much of this variation is due to the personal capacity in which members attend. As a result, outcomes are a product of, among other things, their experience in international negotiations, how much of a mandate they have from the country that nominated them to adopt contentious positions, the strength of their informal relationships, their fluency in English, and how effectively they caucus in blocs. There is often a trade-off, for example, between seniority and technical knowledge.

This feels like a critical moment for international tax governance. The BRICS (or at least China and India) are becoming increasingly confident in articulating an autonomous position that diverges from that of the OECD, and many other developing countries are becoming more confident and experienced in international tax policy. The OECD’s offer of limited but significant participation to developing countries might be seen as a threat to the UN. But with a growing rift between the US and Europe on digital taxation, as well as between the OECD and emerging markets, a committee without US and UK membership for the next four years will have a different centre of gravity, and may therefore be more likely to carve a different path. If these terms still mean anything, the UN committee is now much closer to ‘source’ countries and further from ‘residence’ countries.

Update: The committee elected two co-chairs: Eric Mensah from Ghana and Carmel Peters from New Zealand.