Almost all histories of the international tax regime begin with the League of Nations: from the model conventions issued by its Fiscal Committee in 1928, to the Mexico and London draft model conventions. The latter was agreed by a group of primarily European countries in 1946 at Somerset House, just across the road from where I am now. The League never reconciled the differences between the two conventions, and so the modern history of the regime is usually dated from 1963, when the OECD’s Fiscal Committee first agreed an OECD model bilateral tax convention. For the last 50 years, the OECD model has been the foundational text of the international tax regime, even forming the template for its United Nations equivalent.

While I knew that the United Nations initially tried and failed to pick up the League’s work, the interregnum between 1946 and 1963 is often raced over quite quickly in tax history stories: Sol Picciotto devotes five pages to it in his magisterial International Business Taxation [pdf]. So I decided to sit down in the British National Archives to see what I could find out about this intervening period. The transition from the League to the OECD is important because it is often stated that the OECD picked up and ran with the London Draft, which suited the interests of its members. The Mexico draft, largely agreed among developing countries, fell to one side, according to this account, paving the way for an international tax regime that has a bias in favour of capital exporting states. While I will shed a bit of (sceptical) light on this in what follows, I am mainly going to tell the story through some of the more colourful excerpts from the archives. Today we will look at the UN Fiscal Commission, and I’ll follow this up next week with the OEEC (later OECD) Fiscal Committee to which the baton passed.

Part 1: The “Imperialist” powers’ efforts fail at the United Nations

The sense one gets from both the official reports of UN Fiscal Committee meetings between 1947 and 1951, and the British participants’ own readouts, is that political divisions between groups of states were less problematic than the lack of a clear and compelling mandate to achieve anything in particular. In the committee’s first session, it was the participant from the United States who drafted the proposals for further work that made their way into the final draft, even though he also initiated a protracted (and familiar) discussion about being realistic given limited secretariat resources. Indeed, at the second session, “the secretariat work had been unevenly done and was on the whole badly presented”, said the British participant, WW Morton, who regarded the secretariat’s approach as “over-academic”. (There is a theme of hostility towards things being ‘academic’ in these Inland Revenue files, which I am not taking personally).

By this point, cold war divisions had already emerged, although the sense from the British accounts is that they were not insurmountable, since the Soviet group was content on occasions to make its statements and then abstain from votes, or else be outvoted. Still, here is a flavour of the kind of thing, taken from Morton’s readout. He describes the member from the USSR stating that international work on double taxation put “pressure on the under-developed countries to the advantage of highly developed countries” since it primarily reduced the taxation of their investors.

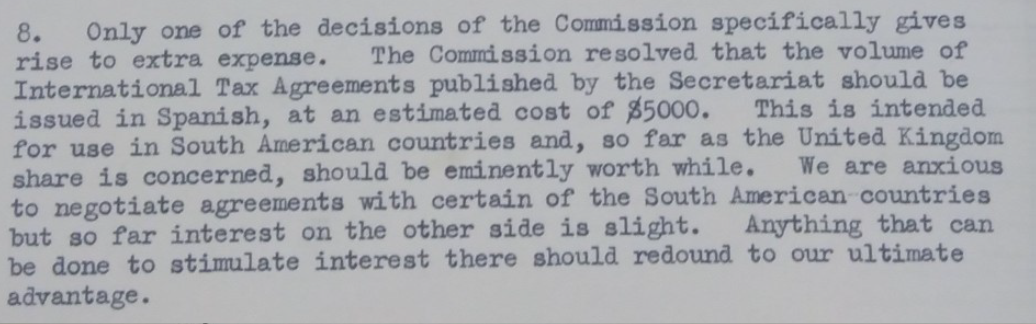

Of the second session, Morton observed that “the session was not very productive” but was keen to support anything that might allow the UK to conclude more tax treaties with developing countries. Everyone could agree to support information gathering and dissemination, and the translation of the secretariat’s compendium of international tax agreements into Spanish was something the British supported enthusiastically, keen as they were to obtain tax treaties with Latin American countries (more on that here).

It is in the Commission’s third session that we can first see a divide between developed and developing countries. The International Civil Aviation Organisation (ICAO) had brought a proposal for reciprocal exemption of airlines, by which companies operating flights would be exempt from taxation in the countries to which they fly, paying it only in the country where they were based. India, Pakistan, Venezuela and Cuba raised objections, pointing out that if only one country signing the treaty had an airline, “reciprocal exemption is quite unfair.” The ICAO proposal was, however, consistent with the treaty policy of the UK, and other countries with their own airlines. The ICAO proposal fell after a vote in which the developing countries were joined by the Soviet group, but Morton attributed this to a “procedural tangle” and poor chairing, rather than an insurmountable division. “As will be observed, the work of the Session was only modestly productive. Nevertheless, it is probably worth holding.”

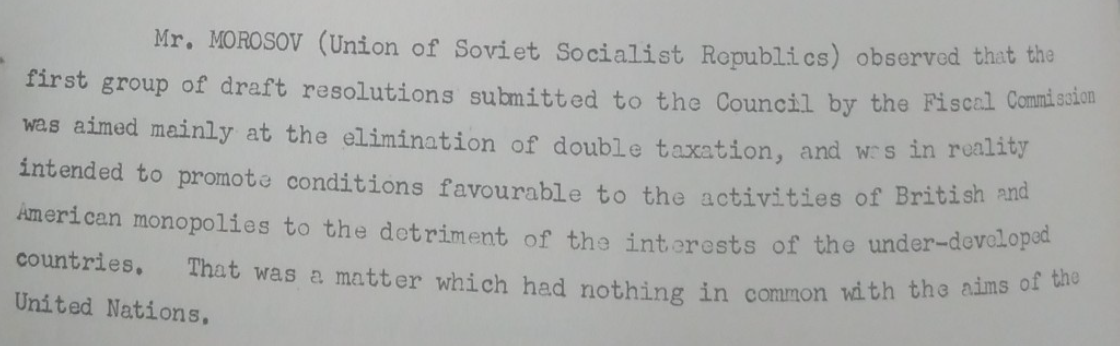

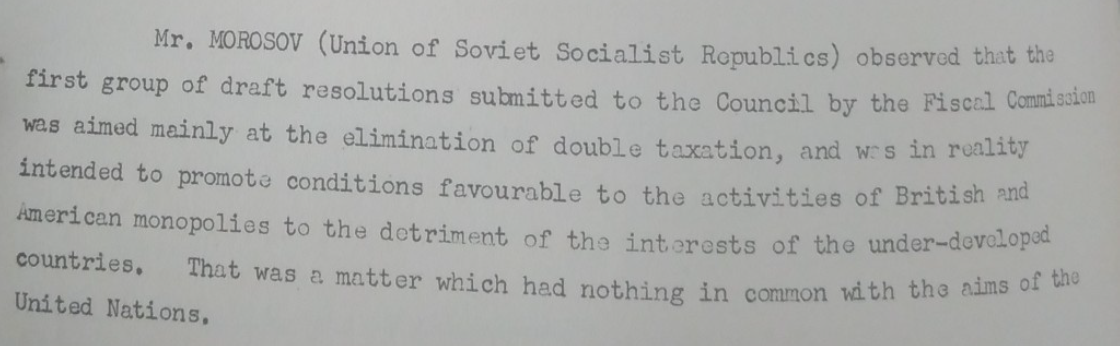

When the Commission’s work reached the ECOSOC, however, it appears that sentiment had changed. Morosov, the Russian participant (also its representative on the Commission itself) expressed his familiar objection that the Commission’s work on double taxation “was in reality intended to promote economic conditions favourable to the activities of British and American monopolies,” concluding that the Commission “was engaged in futile operations, and that it was therefore useless to keep it in existence.” According to his Polish counterpart, “the majority of the Commission had, by certain of the recommendations adopted by that body, tried to exploit the authority of the Economic and Social Council to relieve investors from the highly-industrialised capitalist countries of the taxation which those less highly developed countries were entitled to enforce.”

Morton, the British representative on the Commission, had previously reported an informal conversation with Morosov from which he concluded that this language was more of a formality, and that Russian objections were far from fatal to the Commission. It was thus the British who really plunged the knife in to the Commission, responding that the UK was “in agreement with the Soviet Union and Polish delegations as to the desirability of winding up the Commission’s activities, although for other reasons than those advanced by them.” The UK wanted to see preparatory work for ECOSOC discussions carried out by “small groups of experts with the assistance of the Secretariat,” rather than by a permanent functional commission serviced by a dedicated secretariat. This would appear to have been the death knell for the UN Fiscal Commission, which was wound up in 1954.

So in this quick look through the archives, we’ve seen that the demise of the UN Fiscal Committee was not only a product of inter-country rivalry (though that produced some entertaining diplomatic fireworks). Perhaps more significantly, it was a matter of failure to gather institutional momentum, in part due to the lack of effective secretariat support, and lukewarm support from across the board. The UK and US were never strongly in favour of a permanent international committee examining taxation issues. As we will see in part 2 next week, this was not merely scepticism of the UN: the British also opposed the creation of a “gathering of international chatterers” at the OEEC, which eventually became the OECD Committee on Fiscal Affairs…

Fascinating, thank you!