It’s been quiet on here because of a field trip in Thailand, Vietnam and Cambodia, of which more anon. In the meantime, I’ve been given the opportunity to present a paper based on a chapter of my thesis several times this autumn. It’s a historical study of the politics of Britain’s tax treaty negotiations. I… Continue reading British tax treaties with developing countries, 1970-1981

Tag: United Kingdom

Tax competition: Tax Justice Network and the Oxford University Centre for Business Taxation agree!

The [corporate tax] system allows countries to compete with one another in a manner that destabilises the system itself. Countries compete to attract economic activity and to favour ‘domestic’ companies…Such a goal is not easily reconciled with another goal often explicitly held by governments: ensuring that companies should pay to some country or countries a… Continue reading Tax competition: Tax Justice Network and the Oxford University Centre for Business Taxation agree!

Time we scrutinised China’s tax treaty practice, too

On Monday the UK parliament took a total of 17 minutes to scrutinise new tax treaties with Zambia, Iceland, Germany, Japan and Belgium. I’ve complained before about how paltry these debates tend to be, and was all set for another blog along those lines. There was, indeed, much to grumble about. No questions from the… Continue reading Time we scrutinised China’s tax treaty practice, too

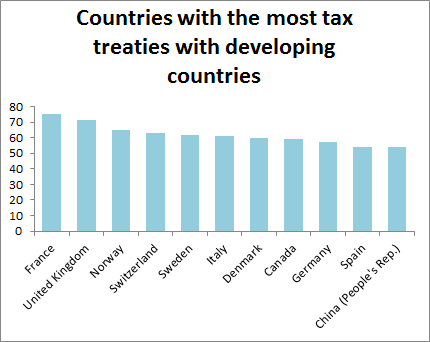

Legislative scrutiny of tax treaties: compare and contrast the UK and US

Here’s an interesting chart. Do you notice anyone missing? Interestingly, the United States is considerably less keen on signing tax treaties with developing countries than you might expect, given the amount of investment from it to, well, most places. Its only treaty with the whole of sub-Saharan Africa is with South Africa. When I looked… Continue reading Legislative scrutiny of tax treaties: compare and contrast the UK and US