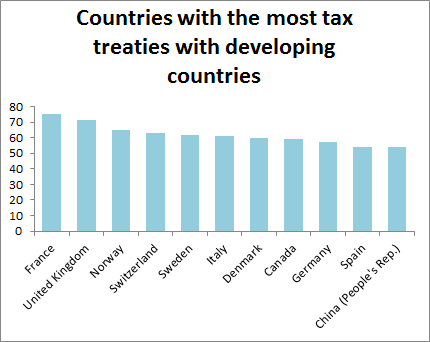

Here’s an interesting chart. Do you notice anyone missing? Interestingly, the United States is considerably less keen on signing tax treaties with developing countries than you might expect, given the amount of investment from it to, well, most places. Its only treaty with the whole of sub-Saharan Africa is with South Africa. When I looked… Continue reading Legislative scrutiny of tax treaties: compare and contrast the UK and US

Tag: David Gauke

The government adopted tax campaigners’ rhetoric at the G8, but much of the status quo is still intact

Here’s my post on the LSE Politics & Public Policy blog. The Enough Food for Everyone If campaign – successor to Make Poverty History – has succeeded in making tax haven secrecy the centrepiece issue of public debate around the G8 summit, which closed yesterday in Eniskillen. It also chalked up a genuine success, in… Continue reading The government adopted tax campaigners’ rhetoric at the G8, but much of the status quo is still intact

Putting a price on the reputation risk from tax avoidance

What are the reputational consequences of perceived corporate tax avoidance? That’s the question that introduces today’s “Tax and Reputation Forum,” organised by the Oxford Centre for Business Taxation and friends. (It’s at King’s College London, so after the High Court the other week, I’m beginning to think that Aldwych is the centre of tax news!)… Continue reading Putting a price on the reputation risk from tax avoidance

Companies are behaving in precisely the way that our international tax system incentivises them to behave

This is my post published on the LSE Politics and Policy blog last week, written before the corporation tax announcement in the budget. It went down a storm with the UK Independence Party’s Financial Services spokesman: @eurocrat @martinhearson @LSEpoliticsblog Half hearted assertions backed by no evidence. As usual academia with no business acumen — Steven… Continue reading Companies are behaving in precisely the way that our international tax system incentivises them to behave