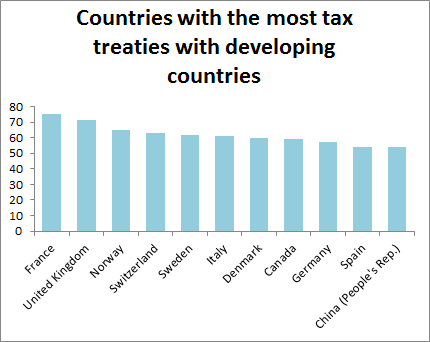

Here’s an interesting chart. Do you notice anyone missing? Interestingly, the United States is considerably less keen on signing tax treaties with developing countries than you might expect, given the amount of investment from it to, well, most places. Its only treaty with the whole of sub-Saharan Africa is with South Africa. When I looked… Continue reading Legislative scrutiny of tax treaties: compare and contrast the UK and US

Tag: United States

Why the US and Argentina have no Tax Information Exchange Agreement

In this new era of automatic information exchange between tax authorities, the United States has come to be seen as the driving force behind the end of tax secrecy. (Although I note that back in 2010 Tax Justice Network said that the US’ FATCA initiative “preserves the essential Tax Haven USA approach – preventing the… Continue reading Why the US and Argentina have no Tax Information Exchange Agreement

Why FATCA might be good for developing countries

Recently I wrote a post explaining that I feel cautious about the burden that compliance with an automatic tax information exchange standard would place on developing countries. Since then a new paper by Itai Grinberg has popped up called Emerging Countries and the Taxation of Offshore Accounts. This amused me. I encountered Grinberg a couple… Continue reading Why FATCA might be good for developing countries

Obama’s reply to the Republicans on closing income tax “loopholes”

Just a quick post today because I’m at a conference. I thought this post on Start Making Sense was interesting. Dan suggests that the political debate in the US on the Bush tax cuts has adopted the language of ‘expenditure’ to refer to this proposed tax cut. It’s an interesting example of how the language… Continue reading Obama’s reply to the Republicans on closing income tax “loopholes”