The [corporate tax] system allows countries to compete with one another in a manner that destabilises the system itself. Countries compete to attract economic activity and to favour ‘domestic’ companies…Such a goal is not easily reconciled with another goal often explicitly held by governments: ensuring that companies should pay to some country or countries a fair amount of tax on their global profits.

– Michael Devereux and John Vella

The effective tax rates on multinational corporations are being pushed steadily downwards, allowing multinationals increasingly to free-ride on the public services that everyone else pays for.

– Tax Justice Network

My term’s teaching is over, which means a return to blogging. Conveniently, several new – and related – papers popped into my inbox this week. There’s “Ten Reasons to Defend the Corporate Income Tax” from the Tax Justice Network, and two from the Oxford University Centre for Business Taxation, “Business Taxation under the Coalition Government” [pdf] and “Are we heading towards a corporate tax system fit for the 21st century?” No love lost between these two organisations, so it’s interesting to see how much common ground they share.

TJN’s paper, written by Nick Shaxson, is typically polemical, smartly designed and peppered with quotes from authoritative sources in support of its case, which is of course that corporation tax is good, and under threat. Shaxson marshals an impressive battery of sources in support of his argument, although the polemical tone, natural from a campaigning organisation, often left me suspecting that the other side of the argument had not been done justice. For example, a lengthy footnote convinced me that “numerous independent bodies have concluded after exhaustive studies that the burden [of corporation tax] largely falls on the owners of capital — that is, predominantly wealthy people”, with a split between capital and labour of something like 75/25. The claim is that numerous, not all, studies find this, and numerous papers are indeed cited, but I still wish that the studies finding a different result had been included, too, even if only to debunk them.

This point came up at the launch event for “Business Taxation under the Coalition Government”, a collective publication of the OUCBT. Chris Wales from PWC, who was a special adviser to Gordon Brown and now advises Labour on corporation tax, was there to suggest what Labour might do in government. When the Treasury minister David Gauke asserted that the incidence of corporation tax falls predominantly on (small-L) labour, Wales retorted that the cut in UK corporation tax rates over the past five years does not appear to have been passed on to workers, given the stagnation in wages over the same period.

Tax cuts in the UK

“The UK’s tax-cutting corporate model since 2010 is a terrible model for anyone to copy – for all the evidence so far suggests that the experiment has been a disaster,” says TJN, citing Reuters research suggesting the creation of just 50 jobs. Because TJN’s argument is about growth, it doesn’t rely on the absence of a link between taxation and investment, and indeed Shaxson is happy to concede the existence of such evidence. His case is as follows:

Many of these studies focus on gross benefits stemming from a tax cut (i.e. they measure investment levels), without also considering all the tax and other costs as outlined in the rest of this document: lost revenue, damage to other parts of the tax system, steeper inequality, greater rent-seeking and externalities, and so on. From the perspective of those designing national tax policies – which is the perspective that matters most – it’s the benefits net of these costs that matter.

The OUCBT report agrees with TJN that it’s near impossible to isolate the effect of the UK reforms on investment, and seems to accept TJN’s point in a footnote to its discussion on the effects of different tax rate measures:

Such measures help in comparing the UK to other countries, but only relative to the costs associated to the corporate tax system: they tell us whether the UK corporate tax burden is low enough to attract and foster investment in competition with other countries, ceteris paribus. They are not suitable to derive conclusions on the broader welfare implications of tax policy measures or on the broader economic performance of the UK.

Earlier on, the report finds an annual tax cost for the next financial year of £7.5 billion, noting that “[b]y any standards, these represent large costs, which must be met either by other taxes raising more revenue, lower spending or a higher deficit. This represents a clear trade-off with the gains in competitiveness.”

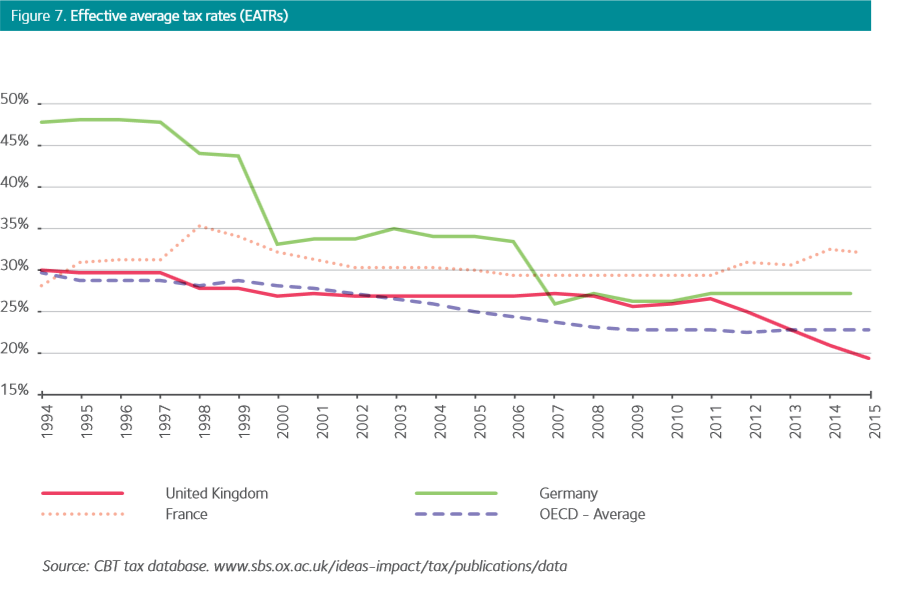

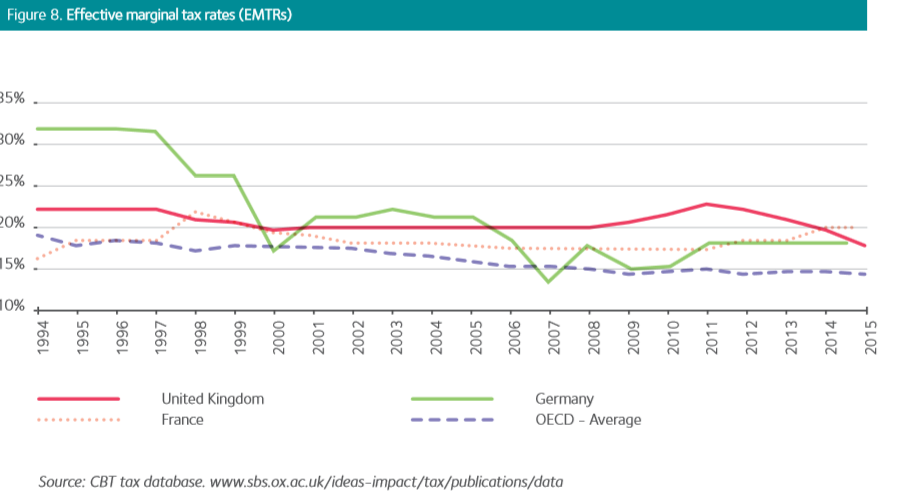

Setting that to one side for a minute, the OUCBT discussion of the effects of different tax rate measures on investment was new to me and certainly interesting. The authors distinguish between three different tax rates:

- the headline rate, which they say is what incentivises profit-shifting;

- the effective average tax rate (EATR), which they say affects the number of investments (the extensive margin); and

- the effective marginal tax rate (EMTR), which they say affects the size of investments (the intensive margin).

The UK is now very competitive in terms of the EATR, but not so much the EMTR. This should have a positive effect on investment into the UK, because,

There is strong empirical evidence that differences in the EATR across countries affect the location of investment projects. The EATR is relevant in a context where a firm needs to decide among a set of mutually exclusive projects. This is the typical decision faced by a multinational choosing to locate investment in one of the OECD countries.

In contrast, the higher EMTR might discourage investment from capital-intensive sectors:

The UK tax component of the user cost of capital (EMTR) has historically been higher than the OECD average and this has not changed under the Coalition. For large companies, the UK capital allowances regime remains one of the least generous in the OECD. This affects firms’ cost of capital negatively, especially for businesses with substantial investment in physical assets such as plant and machinery and buildings.

According to the report, the UK has actually tightened its capital allowance regime for large companies during the past five years. So pointing to headline rates alone is not enough to demonstrate the death of corporation tax. The tax base needs to be considered, and in the UK case changes here seem to have slightly mitigated the impact of the falling rate.

The nature of competition

“Tax ‘competition’ has nothing to do with competition but has more in common with currency wars or trade wars,” says TJN. “We prefer the term ‘tax wars,’ which is more economically literate and more accurately reflects the harm that the process causes.” The OUCBT is a common target for this vein of criticism from TJN (see for example this blog by Nick Shaxson on its origins), and its Business Tax report is certainly laced with the term ‘competitiveness’. But the new paper “Are we heading towards a corporate tax system fit for the 21st century?” by the Centre’s Michael Devereux and John Vella is actually much closer to TJN’s position than one might expect.

The paper examines the OECD’s BEPS process in the light of two criticisms of the current system. First, it argues that the “arbitrary compromise for the allocation of profit between countries first agreed in the 1920s is wholly inappropriate for taxing modern multinational companies.” That discussion is for another day. Its second argument, the relevant one for our discussion here, is that the international tax system is undermined by tax competition, and BEPS will only succeed if it “contain[s] the power of existing competitive forces”:

Recognising the power of this competition is key to creating a stable long-run system for taxing the profits of multinational companies. Even if existing governments were to reach an agreement to preserve the basics of the existing system, while tightening anti-avoidance rules, there will still be an incentive for future governments to undermine that system, as their predecessors have done in the past. A stable system must remove the incentives for governments to undercut each other.

Importantly, Devereux and Vella argue that tax competition is not merely about attracting foreign companies to invest into a country. It is also about giving domestic companies a competitive advantage over their foreign competitors. Both the UK’s Finance Company Partial Exemption and the US ‘Check the Box’ rules are seen in this light, as instruments that confer a competitive advantage on firms headquartered in those countries at a potential cost to the countries in which they invest. The paper even goes as far as to question the “underlying rationale for providing a competitive advantage to domestic multinationals,” since if the beneficiaries are shareholders, many or indeed most of them may be foreign citizens.

A final thought

I’ve compared here three papers, two from academics, who have academic freedom but are nonetheless funded by multinational firms, and one from campaigners who consider the behaviour of those same firms (and to some extent those same academics) to be a threat to democracy and prosperity. They all agree that corporate tax competition is a problem that should be tackled. But they all stand outside the system looking in.

What about those engaged in tax competition? At the OUCBT event to mark the launch of its Business Tax report, Michael Devereux tried and failed to identify some “clear blue water” between the British Conservative and Labour parties. The only difference – at a time when the Labour party is seeking to differentiate itself from the Conservatives as the champion of responsible capitalism and fair taxation – appeared to be a single percentage point on the corporation tax rate. No mainstream political actor in the UK is proposing to move away from the structural changes made to the UK tax system, some of which are characterised by Devereux and Vella as “state-approved base erosion.”

Martin

I’m pleased that you have noted some of our work, but you should be less surprised about overlaps between CBT and NGOs – after all we have collaborated in the past, see

Click to access transparency-in-reporting-financial-data-by-multinational-corporations-july-2011.pdf

I understand that no reference to CBT is complete without a comment on our business funding. But, as I have always pointed out: this comes without any strings attached; we have complete academic independence; we also raise as much money from competitive research grant funding from ERSC and the Nuffield Foundation. Our research and our conclusions are entirely our own. We are neither pro- nor anti-business. I do not believe that there is a single report or paper published by CBT that is not academically rigorous, and supported by data and theory. If you believe any part of our output is biased, then please identify it.

Mike Devereux

PS. John Vella is a lawyer, not an economist.

MIchael, thanks for your comment. As you know, I worked with you on the paper you cite. I did not intend in my comment about funding to make any suggestion about bias or lack of rigour, and hope others have not construed it in that way. I will correct the reference to John Vella.

Martin, this is a really interesting post, and it’s good to see some diplomacy in this (apparently not quite so contested as we thought) terrain. Will write this up for TJN in due course. In response to Mike Devereux’ point about funding, I could pick up on a couple of things but I think that it’s a mistake to frame these things in terms such as “pro-business” or “anti-business” (these are dog-whistle words, see here http://foolsgold.international/competitiveness-the-dog-whistle-words/ ) The main point is that TJN’s whole “10 reasons to support the corporate income tax” document notes that it’s easy to make a pro-business case for the corporate income tax.

although I’m not sure that ‘dog-whistle’ is quite the right term here: scratching my head to think of a better one; all suggestions welcome.