This is the second of three posts in which I’m reflecting on the recent report on BEPS and developing countries [pdf] during a short stay in Africa. Today, I’m looking at the digital economy. This visit to Africa has been the first time I’ve really grasped the scale of what mobile internet is doing to… Continue reading Taxing the digital economy is (going to be) an African issue

Tag: Tax treaty

Time we scrutinised China’s tax treaty practice, too

On Monday the UK parliament took a total of 17 minutes to scrutinise new tax treaties with Zambia, Iceland, Germany, Japan and Belgium. I’ve complained before about how paltry these debates tend to be, and was all set for another blog along those lines. There was, indeed, much to grumble about. No questions from the… Continue reading Time we scrutinised China’s tax treaty practice, too

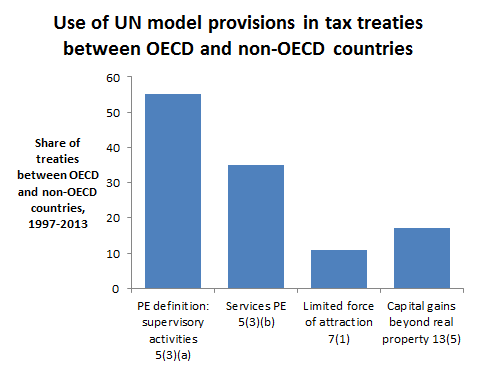

What is the UN tax committee for, anyway?

In January, the UN tax committee sent out a call for submissions [pdf] to the update of its transfer pricing manual. The subgroup working on this update will be drafting additional chapters on intra-group services, management fees and intangibles, all topics that greatly interest developing countries and civil society organisations grouped around initiatives such as… Continue reading What is the UN tax committee for, anyway?

Oxfam goes for the full Tanzi…but is that far enough?

“Revenue is the chief preoccupation of the state. Nay more it is the state” – Edmund Burke I spent the weekend with some old friends from the development sector. One of them, it now turns out, is working for a public relations consultancy. There was an awkward moment when I explained that I was working… Continue reading Oxfam goes for the full Tanzi…but is that far enough?

Legislative scrutiny of tax treaties: compare and contrast the UK and US

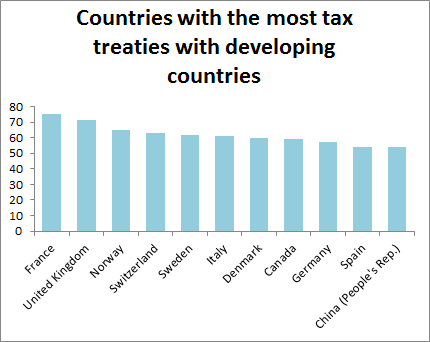

Here’s an interesting chart. Do you notice anyone missing? Interestingly, the United States is considerably less keen on signing tax treaties with developing countries than you might expect, given the amount of investment from it to, well, most places. Its only treaty with the whole of sub-Saharan Africa is with South Africa. When I looked… Continue reading Legislative scrutiny of tax treaties: compare and contrast the UK and US

Some academic thoughts on international tax reform

Since my post last week on unitary taxation, I’ve read a couple of academic papers that give useful perspectives on some of the questions I raised. US states and unitary taxation First up, Lessons for International Tax Reform from the U.S. State Experience Under Formulary Apportionment by Kimberly Clausing. One of the concerns I raised… Continue reading Some academic thoughts on international tax reform