Yesterday a report I wrote for the European United Left/Nordic Green Left (GUE/NGL) group in the European Parliament was published. It was used as input for a hearing of the Parliament’s TAX3 committee, at which Hannah Tranberg from ActionAid, Eric Mensah from the Ghana Revenue Authority and UN Tax Committee, and Sandra Gallina of DG Trade… Continue reading The European Union’s tax treaties with developing countries: leading by example?

Tag: Source and residence

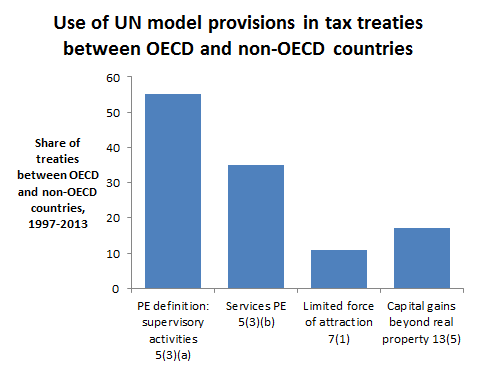

Certainty in the tax treaty regime

Here’s the text and slides of a talk I gave yesterday at an event called Harnessing the Commonwealth Advantage in International Trade. I want to talk today about issues related to tax treaties in developing countries, and their impact on tax certainty for multinational investors. To do this I think we have to consider two… Continue reading Certainty in the tax treaty regime

Policy drift in international tax

The more I think about it, the more I like the idea of policy drift as a way to explain what might at times seem like perverse outcomes in the international tax system. This post is an attempt to road test this idea. Policy drift seems to originate with this 2004 article by Jacob Hacker… Continue reading Policy drift in international tax

Dobbeltbeskatningsoverenskomster!

At the risk of turning this into a travel blog, here I am in Denmark’s parliament building, the Borgen, a treat for aficionados of the TV programme. I spoke yesterday at a hearing organised by the parliament’s fiscal affairs committee on Denmark’s tax treaties with developing countries. The hearing was provoked by ActionAid Denmark’s questioning… Continue reading Dobbeltbeskatningsoverenskomster!

Oxfam goes for the full Tanzi…but is that far enough?

“Revenue is the chief preoccupation of the state. Nay more it is the state” – Edmund Burke I spent the weekend with some old friends from the development sector. One of them, it now turns out, is working for a public relations consultancy. There was an awkward moment when I explained that I was working… Continue reading Oxfam goes for the full Tanzi…but is that far enough?

Have the source and residence principles become redundant?

How typical. You only just get your head round a concept that you learn it’s no longer useful. So it seems to be with the principles of source and residence, based on a thought-provoking conference at the Oxford Centre for Business Taxation last week. To recap. The fundamental problem of international tax is to allocate… Continue reading Have the source and residence principles become redundant?