Here’s the text and slides of a talk I gave yesterday at an event called Harnessing the Commonwealth Advantage in International Trade.

I want to talk today about issues related to tax treaties in developing countries, and their impact on tax certainty for multinational investors. To do this I think we have to consider two aspects of the tax treaty regime: the multilateral norm-setting processes at the OECD and United Nations, and the individual bilateral treaties negotiated by pairs of countries. The key point I want to make is that, at both these levels, the elaboration of a regime that constrains developing countries’ source taxation rights in ways that risk being seen as excessive is not sustainable in the long term.

Consider first the multilateral level. Last week I was reading a PWC document, ‘Navigating the Maze: Impact of BEPS and Other International Tax Risks on the Jersey Funds Industry [pdf].’ It notes that:

Countries are already diverging from suggested guidance from the OECD, which was meant to bring coherence and consistency.

This does not only apply to developing countries, but there is plenty of evidence to suggest that in emerging markets there is a growing dissatisfaction with the OECD approach, as illustrated by the ongoing row over the status of the UN tax committee, and India’s recent financial contribution to its trust fund, which until then had been empty for over a decade.

Here are two quotes that illustrate this sentiment further:

“For developing countries the balance between source and residence taxation [is] very crucial. International tax rules with its preferences for residence based taxation [are] not in interest of developing countries.”

“The global tax system is stacked in favour of paying taxes in the headquarters countries of transnational companies, rather than in the countries where raw materials are produced.”

It seems that, to maintain the integrity of the international tax system as emerging market voices become stronger, countries that favour residence-based taxation will need to accept greater flexibility within the instruments agreed at multilateral level.

Turning to the bilateral treaties that developing countries have negotiated, here I want to introduce you to some research I conducted at the LSE, funded by an NGO called ActionAid. ActionAid used it to inform a campaign that has targeted individual governments and treaties, calling for renegotiations.

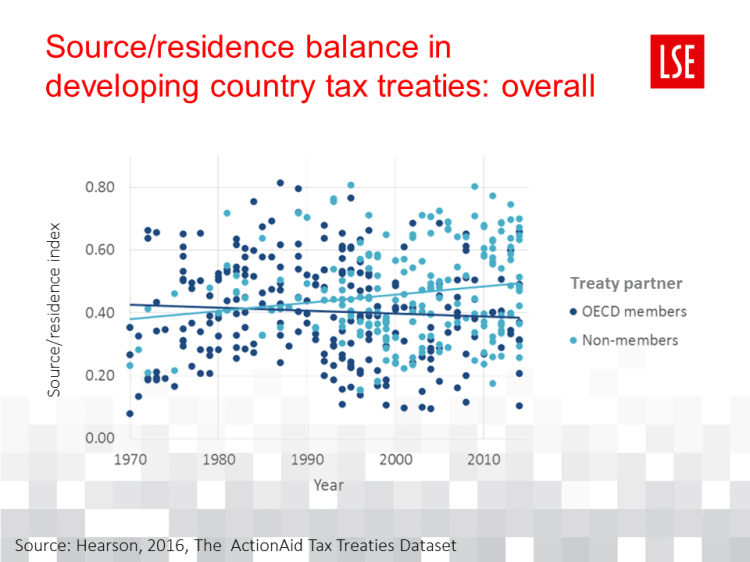

I took 500 tax treaties concluded by developing countries and had a group of LLM students code them for the main clauses that could vary on a source-residence axis, using an International Bureau of Fiscal Documentation analysis. We can use that data to plot each treaty along a simple axis from 0 to 1, where 0 means an overwhelmingly residence-based treaty, and 1 a more source-based treaty. Remember that 1 here represents the presence of the most source-based clauses within existing treaties, and doesn’t take into account the concerns about inherent bias in the parameters for those treaties set by the OECD and UN models. In this first slide you can see that treaties among developing countries, in light blue, are becoming marginally more source-based over time, while treaties between developing countries and OECD members are becoming more residence-based.

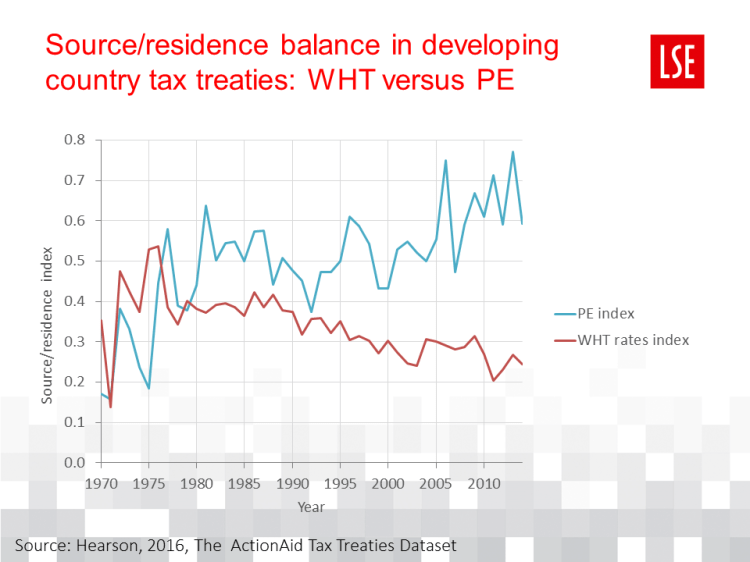

The next chart shows some of the underlying drivers of those trends. You can see that permanent establishment definitions are becoming more expansive, perhaps reflecting changes to the model treaties, while withholding tax rates are trending downwards. There are diverse trends in different clauses within areas such as capital gains tax and taxation of services.

I want to talk to you about a few examples.

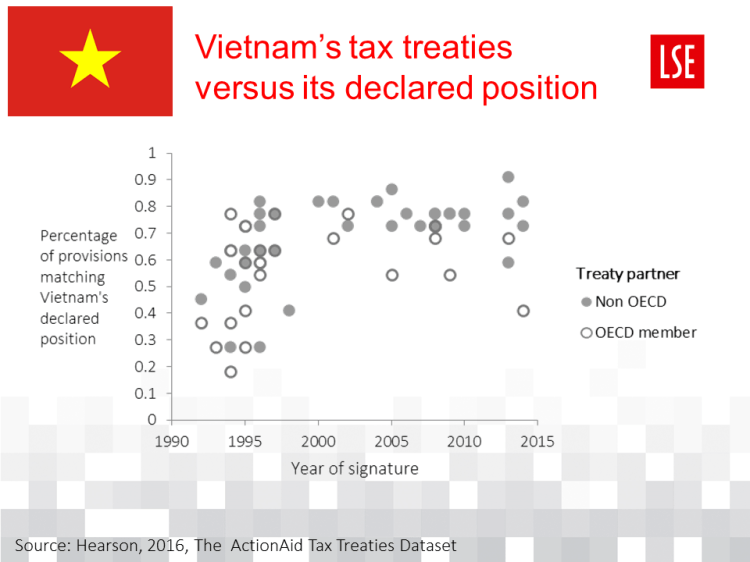

Here we see Vietnam’s treaties taken from the same dataset. Vietnam has actually expressed a comprehensive set of observations on the OECD model convention, broadly following the UN model. So here a zero on the vertical axis means the treaty contains none of those positions and instead follows the OECD model, while 1 means it includes all of Vietnam’s observations. You can see that in the 1990s Vietnam signed a number of more residence-based treaties that are completely the opposite of its stated negotiating position. And of course, these are with many of its biggest sources of investment.

More recently, Vietnam has come to regret those earlier treaties, and has chosen to interpret certain provisions on PE and technical services in the way it wished it had signed them, rather than the way it did. Businesses are very unhappy, and in the words of the Vietnam Business Forum, it has:

made the application of DTA[s] of foreign enterprises impossible, effectively it obliterate[s] the legitimate benefit of enterprises.

The residence-based treaties that Vietnam signed when it was inexperienced and urgently in need of investment are creating uncertainty, rather than the stability that investors are looking for.

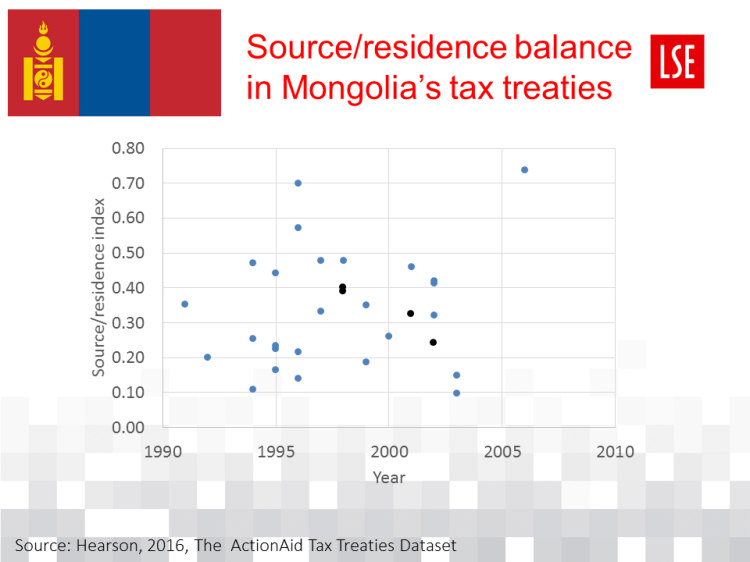

You might be aware that a few years ago Mongolia tried to renegotiate a few of its treaties, and when it was unsuccessful it terminated them. They’re the treaties with the Netherlands, Luxembourg, Kuwait and the UEA, marked in black on here. But if you look on the bottom left, you see a number of treaties with OECD countries, including the UK and Germany, that have even more limited source taxing rights. Indeed, according to an IMF technical assistance report from 2012 [pdf]:

The Mongolian authorities are currently considering cancelling all DTAs and start building up a new DTA network with countries based on trade volumes and reciprocity in economic relations.

I’m told the IMF talked them out of this, but it is worth knowing that they considered it.

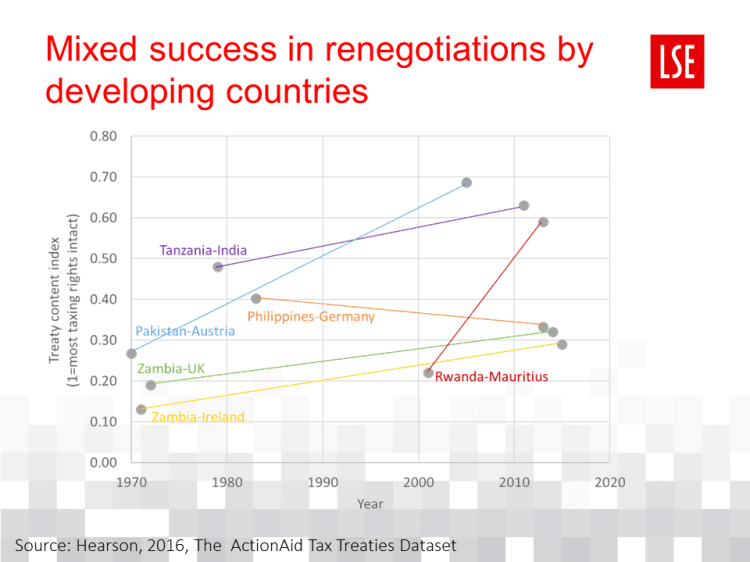

Here is Zambia, a Commonwealth example. You can see the same pattern. Its earlier treaties were very residence-based. I did some archival and interview work on those early treaties, and you can see that when they were first signed, Zambia had a hugely under-resourced civil service, with no experience of negotiation, and other countries took advantage of this. The most egregious example is its treaty with Ireland, which had zero withholding tax rates on all types of payment. That’s in contrast to the East African community countries, which had very strong negotiating red lines, and as a result either walked away, or obtained more source-based treaties that today appear quite generous, but have stood the test of time.

This chart shows a few renegotiations that have taken place in response to government and civil society concerns. You can see that Zambia’s renegotiations have focused more on updating treaties and closing loopholes, not dramatically shifting the balance of taxing rights. In contrast, Pakistan and Rwanda have both negotiated big overhauls.

So in conclusion, as the politicisation of the international tax regime continues, especially in developing countries, I think we’re likely to see growing demands for a rebalancing between source and residence not just in the multilateral setting, but also in individual treaties. My advice to OECD governments, and businesses who engage with them, is that tax certainty in the future depends on an enlightened approach to the tax treaty regime that leaves more developing country taxing rights intact.