In the recent Tax Justice Network Africa report on tax treaties, I had a go at estimating some costs to governments, based on a back-of-the-envelope figure for cross-border dividend and interests payments. This is similar to the methodology used by SOMO and the IMF. (It’s a bit rough and ready, because some of the return on FDI figures I used will include reinvested profits, not cross-border remittances, but I’ve seen some other more sophisticated working recently that produces roughly similar figures.)

What I didn’t realise when I wrote that report is that both Uganda and Zambia break out withholding tax revenue (which includes taxes on domestic as well as cross-border payments) in their budgets, so we can set these very rough estimates in context. I’ve been curious for a while to know the order of magnitude of the importance of tax treaties.

The upshot is that revenue foregone from the lower tax rates on qualifying dividends and interest in tax treaties (which is just one part of the revenue foregone through tax treaties) is about 15 percent of withholding tax revenue. As WHT revenue is about 40 percent of corporate tax revenue and five percent of total tax revenue, this means the revenue foregone is something like five percent of corporate tax revenue, and a little less than one percent of total tax revenue. Here’s how I get there.

Estimating revenue foregone

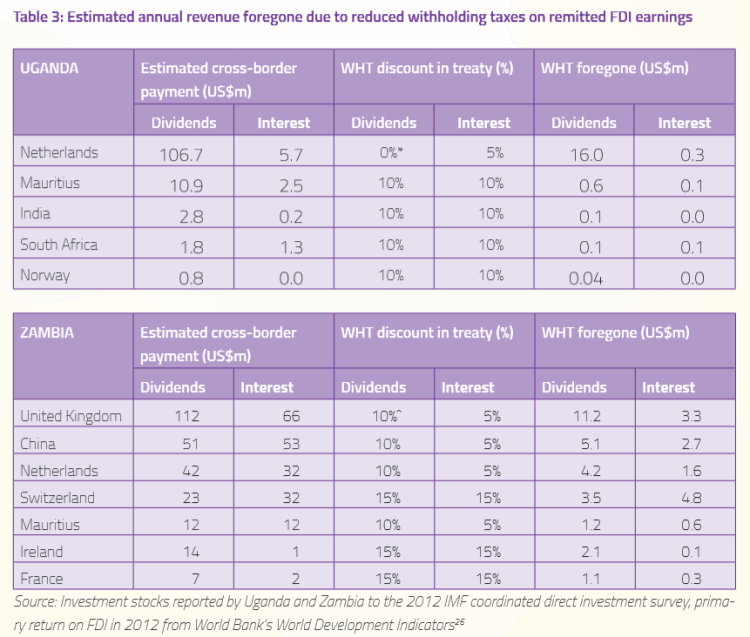

Here’s the table from the TJN-A report. I take figures for the primary return on foreign direct investment and assume that investment from each country gets the same return. Then I apply the tax rate discount in the treaty to that those estimated flows. The revenue foregone using 2012 data is about US$17m in Uganda and US$42m in Zambia.

Uganda

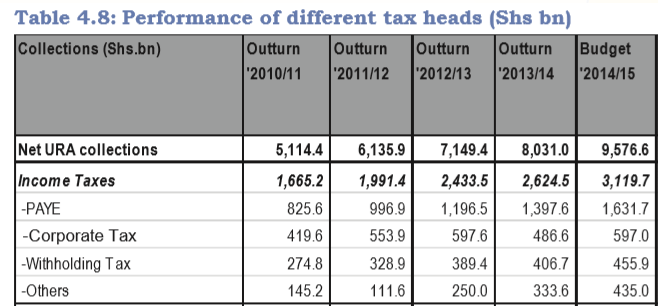

Here’s the table from Uganda’s budget. The 2011/12 withholding tax (WHT) outturn works out at about US$130m using the exchange rate on 1st January 2012. The revenue foregone of US$17m is about 13 percent of total WHT revenue, or 0.7 percent of Uganda’s total tax revenue.

Zambia

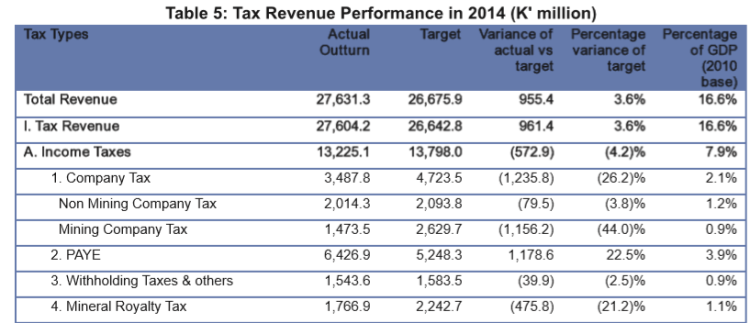

For Zambia I only have the 2014 budget figures, which we can assume with inflation will be larger than those for 2012, the year for which the revenue foregone is estimated, and hence this will be an underestimate of the proportions. WHT foregone of US$42m is 15 percent of the total WHT revenue of US$280m, or 0.8 percent of total tax revenue (using the exchange rate on 1st January 2014).

Since these calculations don’t include the revenue foregone through reduced rates of other withholding taxes on portfolio dividends, royalties and technical service fees, never mind all the other ways in which tax treaties curb taxation of foreign investors, it seems reasonable to conclude that the total of all revenue foregone from Uganda and Zambia’s tax treaties is of the order of several percent of their total government revenue. There may be benefits to offset these costs, but the starting point for a cost/benefit analysis of tax treaties is certainly to estimate the costs!

Hi Martin,

A very interesting exercise – although I did not get how you get the WTH revenue foregone for Uganda? The calculation for Zambia looks straightforward though, so am I missing something obvious? Many thanks for the clarification!

Best, Li

Hi Li, good spot, it looks like I’ve given the treaty dividend rate, rather than the discount, in the fourth column of the table. The statutory rates are all 15% in Uganda, so the discount is 15% minus what’s in that column. That gives the WHT foregone figures in column 6.