I’m at Allison Christians’ brilliant Tax Justice and Human Rights Symposium. Yesterday I began my presentation, as I usually do, by discussing the link between tax treaties and foreign direct investment (FDI). I wrote about this a while ago, but since then I’ve found some more research on the topic. It’s not as simple as saying tax treaties do, or don’t, attract investment. And here’s why.

The story so far

Until 2009, the considered view was that there’s no strong evidence that treaties affect investment, at least not into developing countries. The state of the art was collected in a book edited by Carl Sauvant and Lisa Sachs. Not one of those studies found a positive effect of tax treaties on investment into lower income countries, while they found a mix of positive and negative effects for investment into developed and wealthier developing countries.

There are some intuitive arguments for why the results might be different for developing countries. Tax competition is likely to be less significant in lower income countries, where getting the basics in place (rule of law, transport infrastructure, etc.) is much more important for investors. And large investors can often negotiate bespoke tax incentives that are at least as generous as a tax treaty would have been.

I’m going to give a quick summary of the newer papers. They all use larger or more detailed datasets than in the past to study how a tax treaty between a pair of countries in their sample affects bilateral FDI flows between those countries. I will explain at the end why I think this is the wrong way to ask the question.

New papers using aggregate investment data

Fabian Barthel, Matthias Busse and Eric Neumayer, in 2009 [pdf] found a solid, positive effect of tax treaties on FDI stocks in developing countries, in the region of 30 percent. The main innovation of that paper was to use a more comprehensive set of bilateral FDI data purchased from UNCTAD, and it did seem to make a difference.

Using similar data but a range of different techniques, Arjan Lejour in a recent paper finds that a tax treaty increases FDI stocks between the signatories by 21 percent. He also finds that treaty shopping exists, but doesn’t attempt to quantify how much it contributes to the increase in FDI stocks.

New papers using firm-level microdata

The other papers all use more detailed microdata on the level of individual firms. These data have a couple of strengths. First, they allow us to rule out treaty shopping. Aggregate FDI data generally captures the first link in the ownership chain, as demonstrated by the prominence of tax havens as sources or destinations of investment, when in fact they’re mere conduits. But the microdata tell us the home country of the investor and the final destination country of the investment.

Second, microdata allow the studies to draw a distinction between effects on FDI at the ‘extensive’ and ‘intensive’ margins. Essentially this means the difference between an effect that encourages new companies to invest in a market for the first time (extensive), and an effect that encourages existing investors to put more resources into a market (intensive).

There are four papers. The first, in 2009, was by Ronald B Davies, Pehr-Johan Norbäck and Ayça Tekin-Koru, using data on Swedish firms’ investments abroad. Then in 2011, Peter Egger and Valeria Merlo did the same with German microdata. In a very recent paper, Bruce A. Blonigen, Lindsay Oldenski and Nicholas Sly made use of similar data from the United States. Julia Braun and Daniel Fuentes have also looked at Austrian companies, although they didn’t have access to the same level of detail.

This spread of home countries is important, because it helps to eliminate some of the natural biases in the data, although I think some still remain. To my mind, only the Swedish paper gives us a convincing answer for developing countries: the US only has one treaty with sub Saharan Africa; Austria didn’t sign many treaties with lower income countries; the German FDI data only covers 51 host countries, with a bias towards larger economies and not a single African country.

All these studies agree that tax treaties have effects at the extensive margin, although the effect is not huge. For Swedish firms, a tax treaty increases the likelihood of establishing an affiliate in a country by a small but statistically significant amount – from 0.6% to 0.7%. The German study concurs (its figures vary depending on the variables used). It also includes the effect of the corporation tax rate, and finds this to be much more important. As for the Austrian data, there is more likely to be Austrian investment in a country if there is a tax treaty.

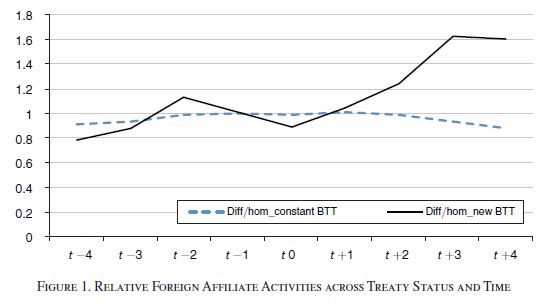

The evidence is less clear at the intensive margin. The German and Swedish studies don’t find a significant effect, while for Austria a treaty does seem to mean a larger number of Austrian-owned FDI projects. This is where the US study comes in. Its main insight is that treaties might affect different sectors differently. It finds that a tax treaty increases both the number of new entrants into a market (the extensive margin) and the volume of sales by a given affiliate (the intensive margin), but only for some firms.

The authors suggest that the attraction to multinationals of a tax treaty is the Mutual Agreement Procedure (MAP), through which countries can settle disputes about who gets to tax them in certain circumstances. Without a treaty, in the event of a dispute the company will most likely be taxed by both countries, because they have no mechanism to resolve it.

They employ a clever test. Internal trade within some firms is dominated by ‘homogenous’ goods for which a price can easily be found, and so (they argue) determining the transfer price will be a relatively uncontroversial affair. The MAP is unlikely to be invoked, and a treaty is not so important. In contrast, firms trading in ’differentiated’ products are more likely to want a treaty to be in place, because pricing these goods is a more subjective business.

This chart illustrates this finding. Three years after a tax treaty with the US comes into force (t0), there’s a big increase in the share of activity in the treaty partner by US companies dealing in differentiated goods, compared to those dealing in homogenous goods.

Why I’m not yet convinced

I said I’d add my own thoughts on this data. Well, to begin with, there’s still the old ‘endogeneity’ question. Do treaties lead, or follow, surges in investment? Studies tend to deal with this by lagging the data by a certain number of years (they ask how much investment there was in, say, year t+1 when a treaty was signed in year t – Lejour’s paper uses time lags as long as six years). From my own research, I know that treaties are often intimately linked with particular large investments: a company planning a big investment will lobby for a treaty. Firm-level microdata should be particularly sensitive to this kind of process. But if the investment decision-making and the treaty lobbying are happening simultaneously, it’s impossible to use the chronological sequencing to untangle whether the treaty influenced the firm’s decision, or whether the firm had already made up its mind to invest.

But the more important point is this: what’s the policy-relevant question? Based on these papers I feel comfortable saying that tax treaties do influence bilateral investment flows. A treaty between A and B is likely to increase investment from A into B. But B doesn’t want more investment from A particularly, it just wants more investment. My own research leads me to believe that tax treaties are often instruments to make firms from A more competitive in B relative to firms from C, D or E. If that is the case, B needs to be sure that any new investment stimulated by a treaty doesn’t simply come because firms from A are outcompeting those from C, D and E; investment from A should be additional to, rather than at the expense of, investment from those other countries.

So actually we want a more blunt study: the effect of signing a new treaty on aggregate flows of investment into a country. The only study to date to have examined this is by Eric Neumayer back in 2006. He found that treaties had no effect. So if we combine this with the studies discussed above, the evidence seems to support the idea that tax treaties change the composition of home countries investing in a country, but not the overall volume of investment. If that’s right, then the answer to the policy-relevant research question is no, treaties don’t attract investment.

NB: It’s worth adding in an additional outcome from the Swedish study. Davies and Norbäck didn’t find any effect of tax treaties on the size of investments (intensive margin) but they did find that a tax treaty caused firms to export less back to their parent companies, and to import more inputs from their parent companies; these effects were stronger for affiliates that didn’t trade with the parent company as their main purpose. They interpret this change as profit shifting, which they argue is because the affiliate incurs a higher effective tax rate once the host country is able to gain information through the tax treaty. I find that interpretation hard to stomach: if firms are taxed more with a treaty in place, the whole argument for treaties would seem to have been turned on its head. It’s a puzzling finding.